looking forward at inflation

US government debt - sold as Treasury Bonds to fund our federal budget deficits - are regarded by the world as a “risk free” asset - meaning there is no chance of losing money from the investment through default. In reality there is no such thing as a “risk free” asset, but T-Bonds are about as good as you can get.

With a regular 10 year T-Bond, you pay for the bond and for the duration of the bond’s life you receive semi-annual “coupon” payments and at maturity you receive the face value of the bond back. So if you bought a bond with a $1000 face value bond, with a 6% coupon rate, you would receive $30 every six months (6% x $1000 divided into two payments of $30 each), and at maturity you would receive $1000.

Without getting into a full lecture on bond valuation, let’s just think about that $1000 that, with a 10-year bond, you would be getting 10 years from now. That’s a long time, and with inflation, that $1000 isn’t going to buy what it would have if you had kept it in your pocket. Let’s say inflation is 3% per year for 10 years. The purchasing power of your $1000 in 2032 would actually be about $744. So even though you are absolutely going to get the $1000, it isn’t going to be worth $1000 in purchasing power. Because investors know this, they balance the loss of purchasing power on the face value of the bond with demanding a higher coupon rate over the life of the bond.

But what if we could account for inflation directly? Enter the Inflation-Protected Treasury Security (TIPS). With a TIPS bond, the face value of the bond increases each year by the amount inflation is recorded at. So if inflation is 3% during the first year, the face value is increased from $1000 to $1030. Over the course of 10 years, if inflation was 3% per year, the face value payment you would receive at the end would be about $1344. Because investors know that they will not lose purchasing power on their face value payment, they are willing to accept a lower coupon rate - they adjust their coupon rate down by the amount they think inflation will be.

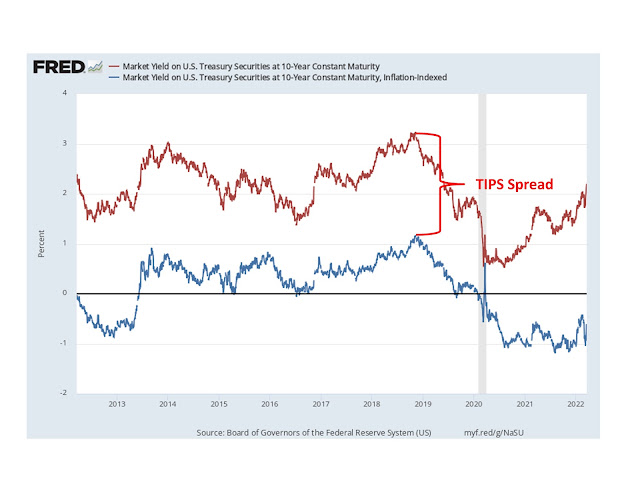

So with all that said, the graph above shows the difference in coupon rates between the regular 10-year T-Bond and the TIPS 10-year T-Bond. The difference between the rates is called the TIPS Spread and it tells us what investors think inflation will be over the next 10 years. What’s important about this spread is that the only way you get to influence this spread is by buying or selling these bonds. So there is real money on the line here, real skin in the game, not just some talking head (or someone writing a newsletter).

As of Friday, the TIPS spread was 2.93%. It has increased steadily but not dramatically, so this tells me investors are still projecting inflation will be transitory - i.e., it will settle back down and return to the historical average. I will be watching the TIPS spread myself for hints about the future. You can watch it too by clicking on the link above.

Comments

Post a Comment